Are Pensions a Complex Pyramid Scheme?

Are Pensions a Complex Pyramid Scheme?

How to understand and avoid them

How to understand and avoid them

I have 1 apple, but my pension provider charged me 1.08 apples to manage my pension this year. I’m suddenly in debt 0.08 apples on the profit earned from my money. It’s enough to leave any mathematically-gifted child scratching their head.

With that, I welcome you to the complex nightmare of pensions… The world’s most accepted pyramid scheme.

Let’s start over. In 2008, many hard-working people lost their pensions in the financial crash and the recession that followed. Despite working and paying in for 40 to 50 years, their reward was nothing or significantly less than they paid in. The system failed them. The same system could fail you too.

Private pension funds are usually an amalgamation of stocks, bonds, derivatives etc and are commonly referred to as low-risk investments. The problem is that when the system fails, it all fails. Even low-risk is a risk.

Bailed out by the government, financial institutions saved their skin, but it was people like you and me that lost the most. My hope is that as we uncover the pyramid scheme behind pensions, you’ll seek out your own investment opportunities and diversify your hard-earned capital for a relaxing, bright future.

What is a pyramid scheme?

A pyramid scheme or ‘Ponzi’ is a “system of making money based on recruiting an ever-increasing number of ‘investors’.”

In this example, as it related to pensions, the more workers the system can recruit, all paying into the system, the easier it is to support those at the top of the pyramid, ‘cashing-out’ at retirement age.

Helpful Behavioral Economics Concepts for the Business-Minded | Data Driven Investor

In corporate America, Gaussian statistics, deterministic interpretations of the world around us, and rational…www.datadriveninvestor.com

The top tier (also known as retirement in this case) can pay-out a huge lump sum based on the cumulative wealth accrued by everyone underneath them, who are still paying into the system.

It works, so why is this a problem?

We’re not dying quick enough

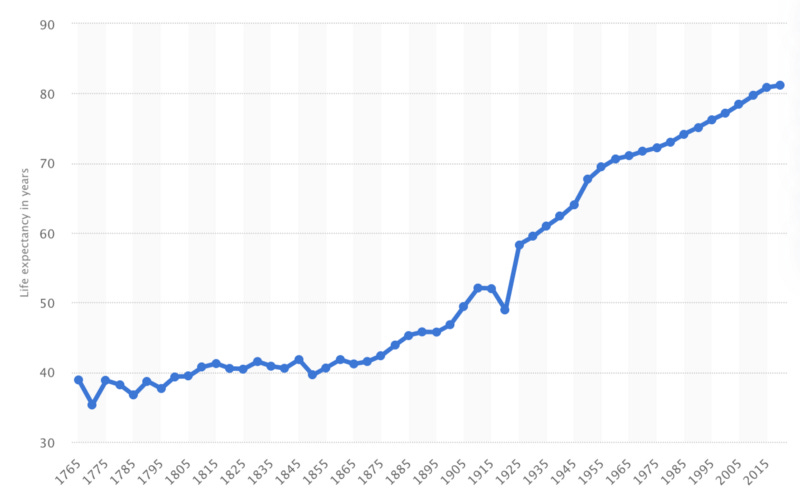

Thanks to medicine, science, technology, innovation and sanitation we’re living longer lives than ever before.

Infant all-cause mortality is down too, so that increases the average life expectancy to far higher numbers than it’s ever been. More people are surviving… and for longer.

This utopian dream of extending life-span puts a burden on the financial sector. If you retire at 65 and live until you’re 81, the government or private financial institution is liable to sustain you for 16 whole years.

Given that the average UK retiree spends £27,000 per year ($35,000), you’ll need to ensure your pension fund is worth £432,000 or more than half a million US Dollars.

Let’s get serious…

It’s been reported that 35% of eligible working people don’t have a pension plan at all. My guess is the number is much higher, the problem with these studies is that they don’t account for the participant's ability to lie — to not feel inadequate in front of the person asking the question.

Even so, that would still show that more than 1 in 3 people will be dependent on tax-fulfilled ‘state pensions’ or ‘social security’ governmental support… Putting a tremendous pressure on every country’s economy.

This, in turn, increases the demand for governments to have more people paying tax into the system than they have people financially dependent on them.

That, in itself, is the definition of a pyramid scheme.

We’re also not making babies fast enough

The need for more people to pay into this pyramid scheme requires more people of eligible working age and health.

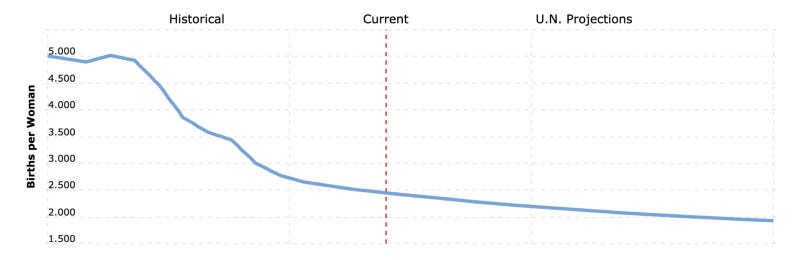

The population of Earth is growing, but overall that data is skewed by the people that are living longer — actual births are declining.

Unfortunately, the U.N. is projecting that global fertility will continue to decline too. The red line on the graph (below) shows our current year as 2020. Before that line is historical data on fertility and after that line are the projections on the continued trend.

Even Elon Musk is worried, tweeting about how overpopulation isn’t an issue.

“Real issue… an aging & declining world population by 2050” — Elon Musk

We’re heading for an inverse-pyramid. Countries that have more dependents than those healthy and eligible enough to work to support them.

The easiest solutions for governments is to change the requirements for ‘drawing down’ a pension. This has taken the form of increasing the age of retirement to age 67 by 2026. However, it’s likely to increase beyond that to offset the need for more workers paying in.

The government’s fight against this problem

In 2012, the UK government enforced a new initiative of Automatic enrolment aiming to put a bigger dent in this problem. “It makes it compulsory for employers to automatically enrol their eligible workers into a pension scheme.”

This forced pension fund is a way to guarantee eligible workers to pay-in unless they choose to opt-out.

Why did this need to be done?

The truth is, nobody has any money. A recent study found that 1 in 10 Brits have no savings at all — and 33% of us have less than £600 in savings, which is a scary statistic.

Moves like this, by the UK government (but replicated by many other countries) along with an ever-increasing retirement age threshold, ensure that people don’t become ‘state-dependent’ in their older years, reducing the burden of government support.

So why have a pension? The good, the bad and the ugly

If it’s a pyramid scheme, with moving bureaucratic-goalposts and an element of risk associated with it, why should you have a pension at all? First, let’s start with the basic-economic cons to having a pension, void of all emotion and compassion.

Their growth is dependent on market growth — stocks, bonds, real estate etc. You could end up with more than you paid in, but it could equally be much less.

They’re subject to fees for ‘management’ of that fund and the profits accrued by it.

You pay taxes anyway, making you eligible for ‘social security’ or ‘state pensions’. Why pay twice?

If you’re in need of private care when you’re elderly, clever investors will have to use their pension or personal savings to pay, whereas frivolous patrons will get that care government-funded. ie. You paid twice. Once (tax) for others who can’t afford to get the care, and once (pension) for you to get the care. Is that really fair?

When you die, it dies. If you pay your pension contributions into a ‘single life annuity’, payments can stop unless there was a ‘guaranteed period’ outlined. However, this is usually only 5 to 10 years as standard.

The income taken out of a pension fund (that you’ve already paid tax on) to buy assets, or create further investments will count as part of your estate when you die. This means it’s potentially subject to inheritance tax or further income tax for a partner or spouse who wants to collect it — if they’re under retirement age.

The proof is in the pudding

Hilariously, I got this letter recently from AVIVA to show how my pension is coming along. I wanted to make sure I shared it with you. It makes that whole ‘apples’ analogy at the beginning of this post make sense.

As you can see from the photo below my pension investment gained, excluding payments in, £5.94 ($7.64) and I was charged £5.99 ($7.70) for the pleasure. They took all my profit and more to ‘manage’ my pension.

What is the solution?

Even if you religiously pay into a pension scheme all of your life, 26% of men and 19% of women (globally) don’t live to retirement age anyway.

That means 1 in 5 women or 1 in 4 men will never see the fruits of their labour.

The solution then is personal savings and investments. Instead of paying a financial institution, bank or pension provider to gamble your hard-earned money with no consequence for them, take control of your own assets.

Remember, it’s important to diversify. Don’t have all of your eggs in one basket. By varying your savings amounts across a myriad of different investments, you’ll be somewhat shielded if one ‘tanks’.

Look at gold’s incredible rise, at the same time the US Dollar (traditional FIAT currency) is plummeting.

By varying your self-managed portfolio across many areas of investment, you’ll be insuring yourself for a less violent loss, should one area fall.

Start researching into investing in assets like:

Gold, Silver & other precious metals

Real Estate

Cash

Jewellery

Bonds (secured, government-backed and with attractive exemptions)

Stocks (selectively, perhaps those that pay regular dividends, or are super low-risk index funds — at least the profit is 100% yours)

Businesses that you can co-own with your beneficiaries.

Essentially you’re looking for appreciating assets, things that are likely to gain value over time. It’s what the pension providers or banks do with your cash in traditional pension funds, except they keep a big slice of the profits and charge you for the privilege of lending them your money.

Break-free from the convenience you find at your feet and start to take ownership of your own future. Nobody will be as motivated for your success as you will be.

Gain Access to Expert View — Subscribe to DDI Intel